Basel 3.1 implementation in UK delayed… once again

Basel 3.1 represents the final set of international banking reforms in response to the Global Financial Crisis. The reforms aim to enhance banks' risk measurement and capital requirement calculations, striving to make capital ratios more consistent and comparable across institutions.

But in consultation with HM Treasury, the PRA has decided to delay the implementation of Basel 3.1 in the UK by one year, to 1st January 2027. This adjustment was proposed to allow the regulator for additional time to observe the rollout of the reforms in the United States.

The delay appears to stem primarily from the potential impact on proposed reforms of the Fundamental Review of the Trading Book (FRTB) front, which includes revised boundaries between trading and banking books, a more sensitive standardised approach for Market Risk, and the introduction of the Non-Modellable Risk Factors charge. Whilst this affects primarily banks with significant trading or investment banking activities, the regulator has chosen to take a comprehensive pause of the entire Basel 3.1 regulation to reassess the entire suite of reforms.

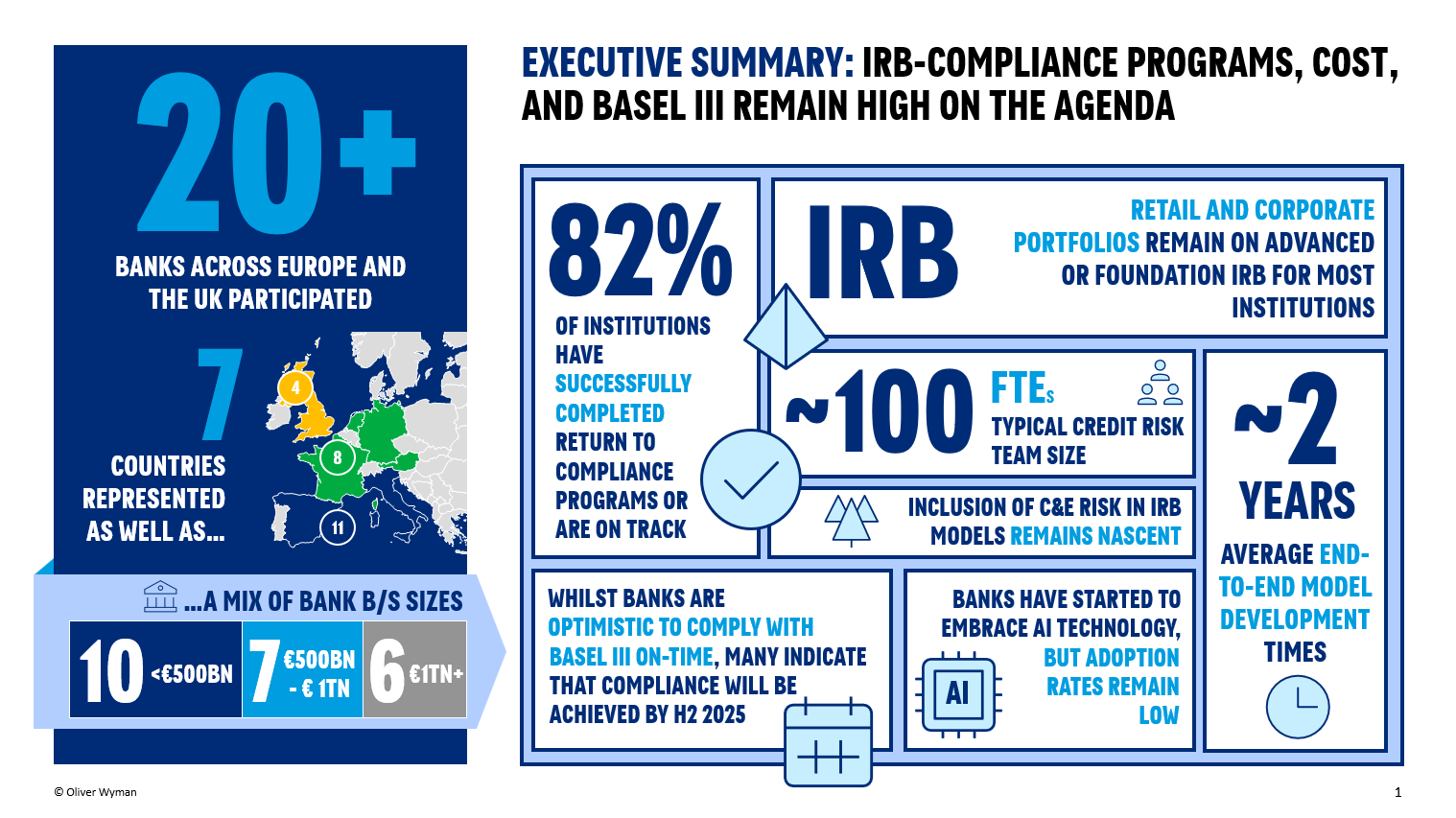

But the reaction from more traditional banks in the UK with significant Credit Risk exposure is mixed. In our latest European IRB survey, clients reported that the new set of rules could lead to potential capital release for some of the Standardized Approach (SA) and Foundation Internal Ratings-Based (FIRB) portfolios. Conversely, firms with significant Advanced Internal Ratings-Based (AIRB) portfolios have deemed the approach conservative and have welcomed the delay.

On the other hand, our belief is that the PRA will be less lenient regarding day-one compliance, as the regulatory text has been available in draft form since 2022. It is also notable that the model output floors have remained unchanged. This means that once the rules come into effect in 2027, banks will need to achieve the required levels of capital by 2030, effectively shortening the transition period to two years.

Another greatly understated driver of the delay might stem from concerns about stifling the British economy, which has struggled to regain its footing post-COVID, with more stringent prudential regulation.

This push ‘from within’ has been already observed elsewhere: Across the pond, Jay Powell, Chair of the Fed, commented back in 2024 that ‘broad and material changes’ were coming to the proposed Basel Endgame framework. Republican lawmakers have consistently expressed scepticism about the reform and have repeatedly called for the program to be scrapped.

The ‘Endgame’ is set to become effective on 1st July, 2025. However, the new administration holds the future of the American banking regulatory landscape in its hands: Trump might push to simplify the reform or scrap the framework completely.

Many domestic banks, lacking international operations, may advocate for abandoning current proposals in favour of frameworks that better suit the American context. On the contrary, recent bank failures have cast doubt on the resilience of smaller regional firms in the US, potentially strengthening the argument for a stricter framework aligned with international practices.

Closer to home, Continental Europe seems to be taking the middle ground, as the Basel 3.1 rules became effective, with some modifications, in January 2025. But the most interesting point is that the FRTB part of the regulation has been pushed back 1 January 2026.

On the Credit Risk front, a 2023 ECB survey determined that corporate-oriented financial institutions would be the worst hit by the reforms. While some capital release is expected from the model outputs, the output floor means that the overall benefit is negated in full.

This puts the EU on an alternative, steadier path compared to the uncertain US and hesitant UK approaches.

This disparity of rules require transcontinental banking institutions to dedicate increased resources to ensure compliance in the US, the UK, and Europe. Future-proofing activities and ensuring that the ability to act quickly remains in place in case new short-term steer emerges from the regulators will be fundamental to ensure risk transformation projects remain compliant once implemented.

Some questions remain unanswered: will the US scrap the FRTB reforms completely? will the PRA modify the ‘near final’ regulatory text to align with the Fed? will Europe continue in its sure path towards complete Basel IV adoption?

For now, we’ll just have to wait and see…

Co-authored with Cian Mellett

Matias Coggiola is a Manager at Oliver Wyman and specialises in Credit Risk modelling methodology and regulatory compliance. Prior to consulting, Matias spent several years as an industry practitioner working within a range of financial institutions across three continents. Matias joined Oliver Wyman in 2024 to help expand the Risk Delivery capability.

Cian Mellett is a Manager at Oliver Wyman and specialises in the development of Credit Risk models. Prior to joining Oliver Wyman, Cian worked for an Irish consultancy delivering a suite of credit risk models for Irish Pillar Banks across multi-year programs. Cian joined Oliver Wyman's Risk Delivery Team in 2024.