Dear all,

Thank you again for joining the recent Oliver Wyman UK mid-sized banks IRB Roundtable. We really appreciated the openness of the discussion and have attached the materials shared during the session for ease of reference.

A few themes stood out from the conversation:

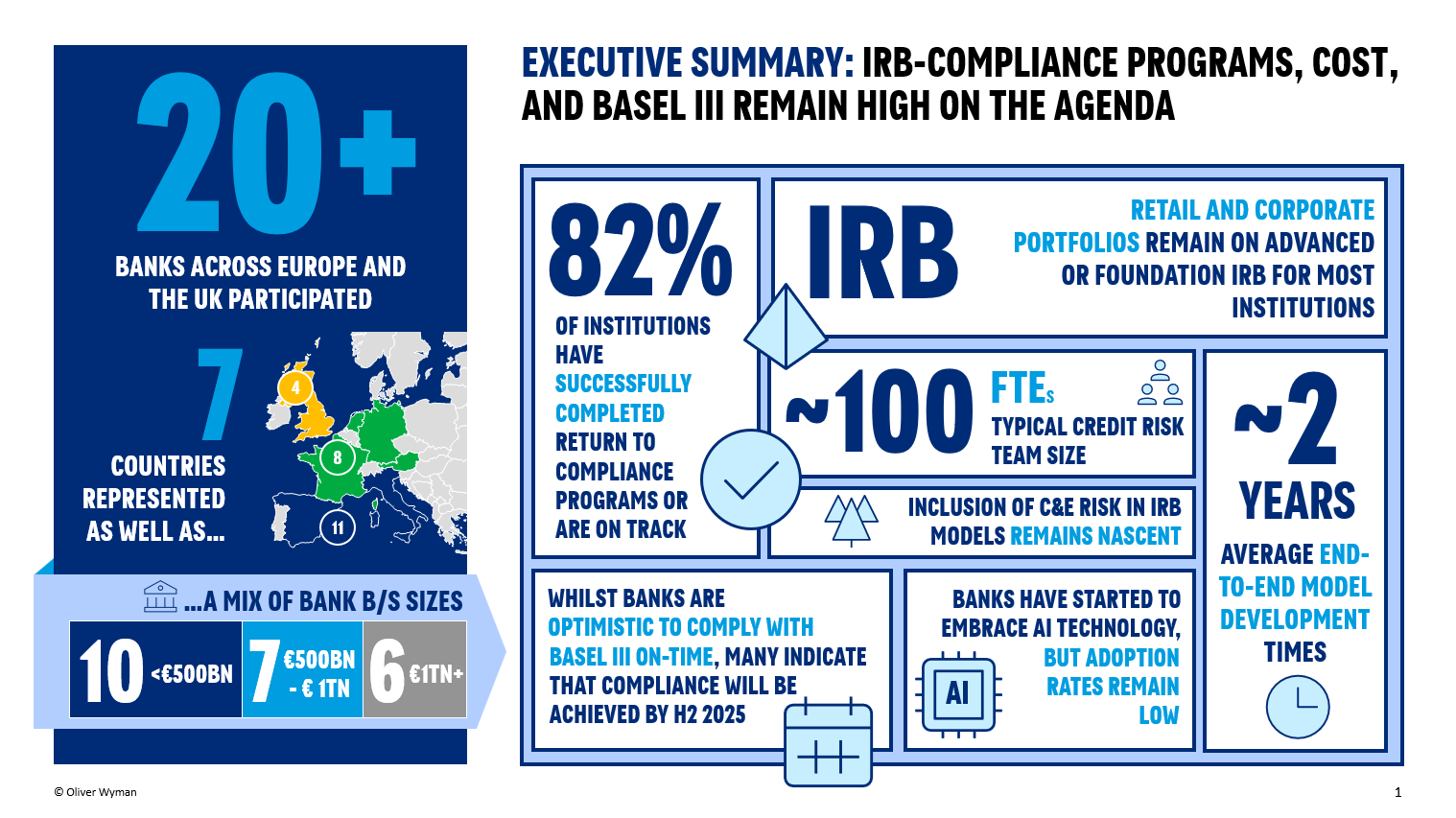

For the mid-sized banks, the IRB journey remains challenging not only from a modelling perspective, but also in terms of building and sustaining a clear internal business case, especially with the upcoming RWA output floor

The value of IRB is seen beyond capital benefits alone, with greater emphasis on stronger risk management, pricing and decision-making

Data continues to be a major constraint, particularly in relation to limited historical depth and LGD data gaps (including collateral valuation)

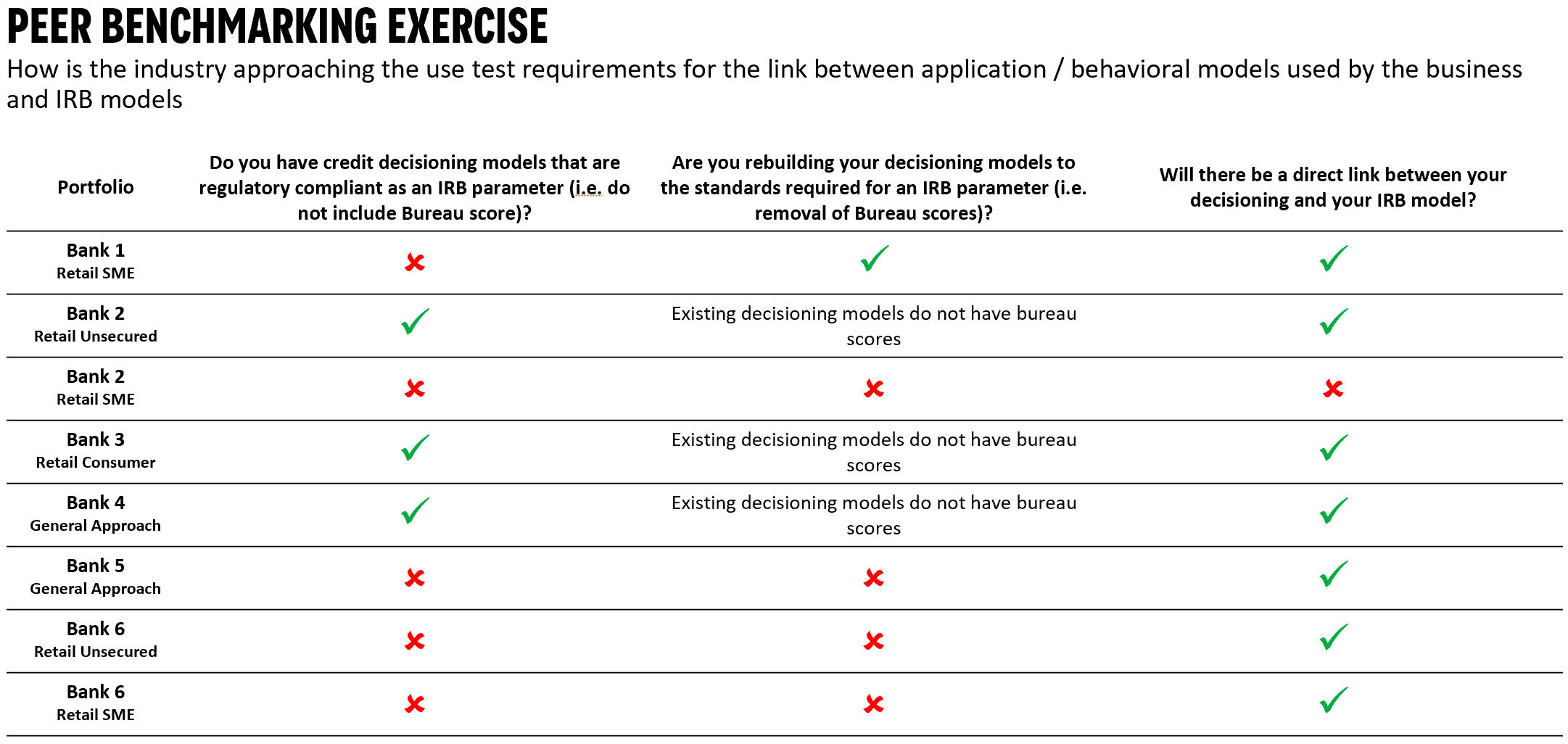

There was strong interest in pooled data, benchmarking and external datasets, although it is important to ensure governance, comparability and validation through a third party engagement

Regulatory engagement continues to be lengthy and complex, especially where expectations around submission completeness are evolving, although there appear to be some recent improvements in supervisory capacity and process

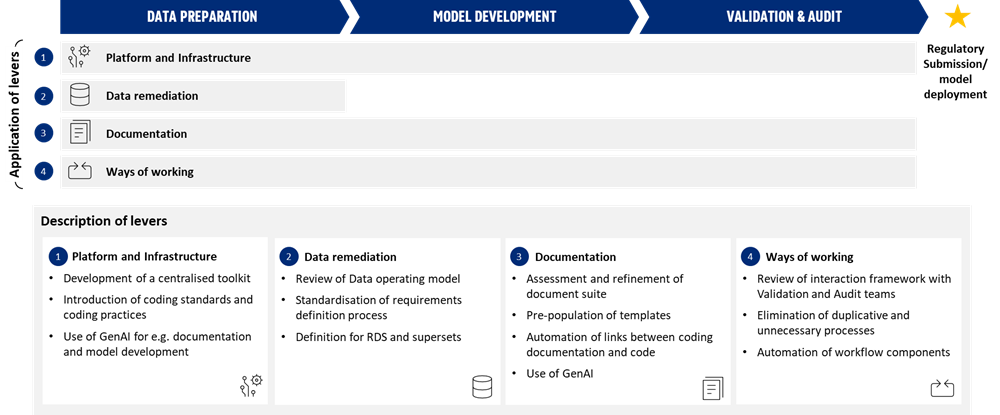

Standardised tooling can help accelerate delivery and improve consistency, but it must remain flexible enough to reflect institution-specific portfolio characteristics and modelling choices

The value of such tooling increases with the validation of such tooling by a third party

Across both modelling and validation, internal ownership within each bank remains critical, particularly for senior modelling leads

Looking ahead, many participants expect validation capacity to come under increasing pressure, especially as models become more complex and increasingly AI-enabled

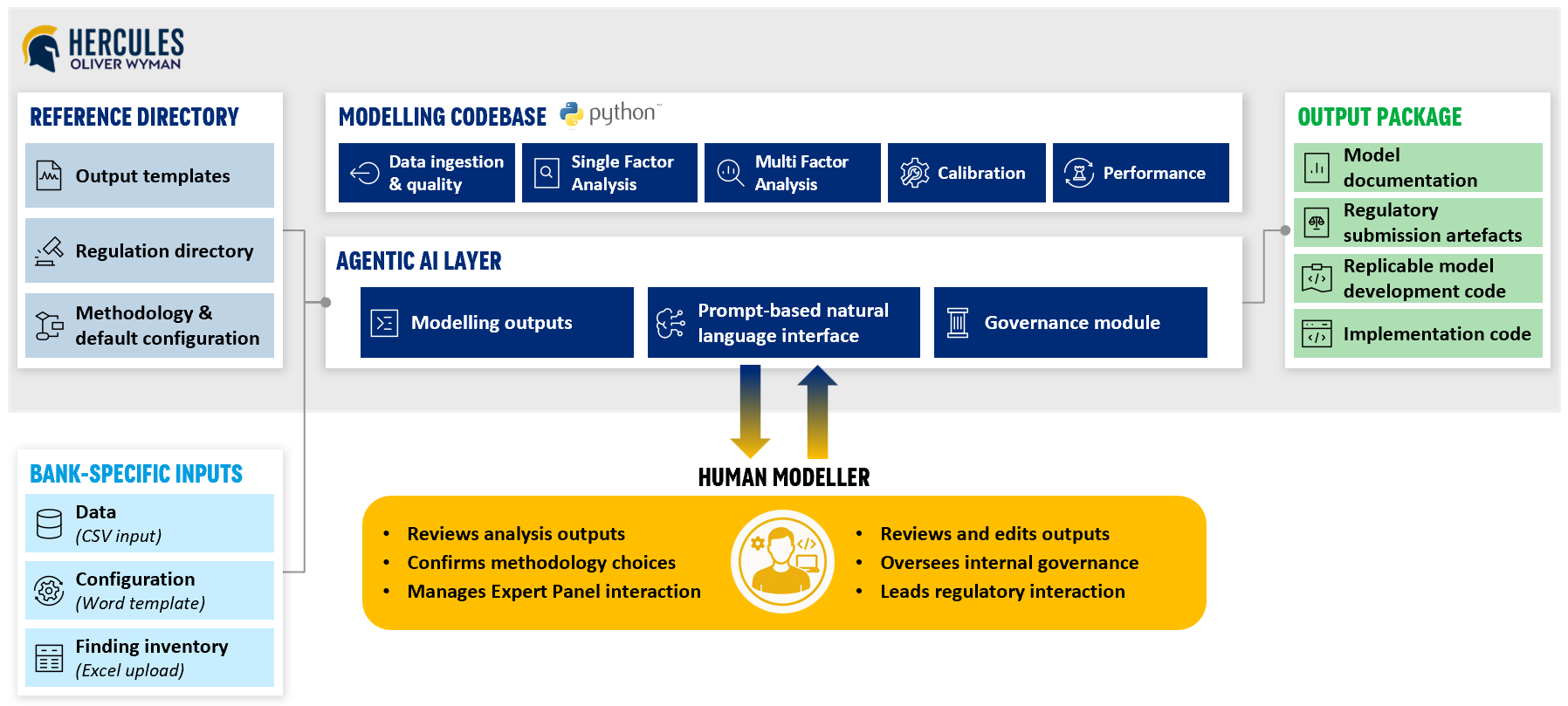

As discussed during the roundtable, we will follow up with more concrete thoughts on practical next steps for data pooling. In the meantime, we would be pleased to arrange a short demo of Hercules, our credit risk modelling toolkit (you can find more details about it here)

Thank you again for the candid and insightful discussion.

Kind regards