Use test requirement benchmarking survey

-

We have been discussing with a UK based client the role of application/behavioural scorecards (used for credit decisioning) and the use test link required in IRB models that are being submitted.

The main concern is around embedding business decision making scorecards as an

IRB parameter when these scorecards typically:- Contain 3rd party bureau scores (PRA have raised concerns around their use in IRB models)

- Can have more advanced modelling techniques

- Are updated more frequently than the IRB models they feed into (breaking the link)

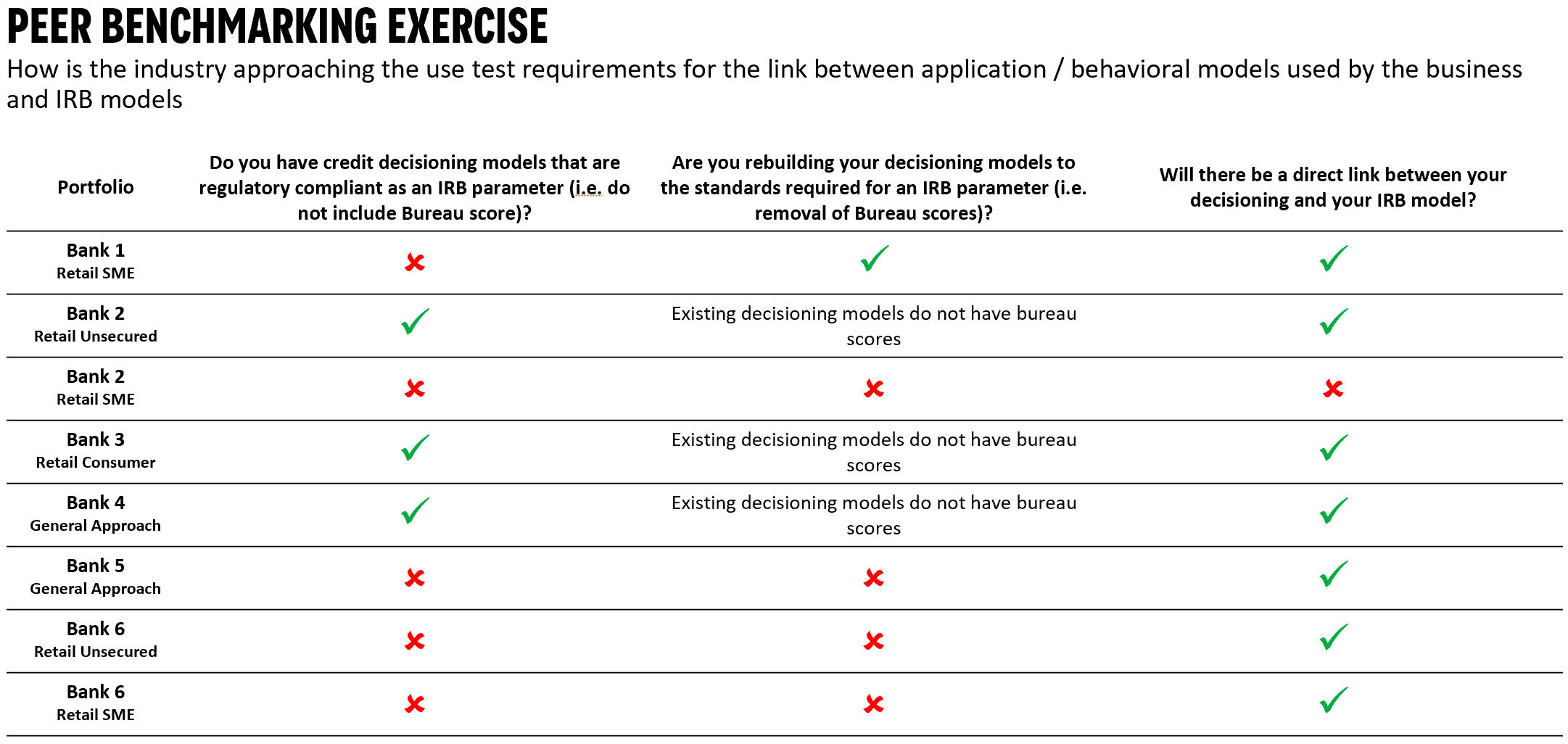

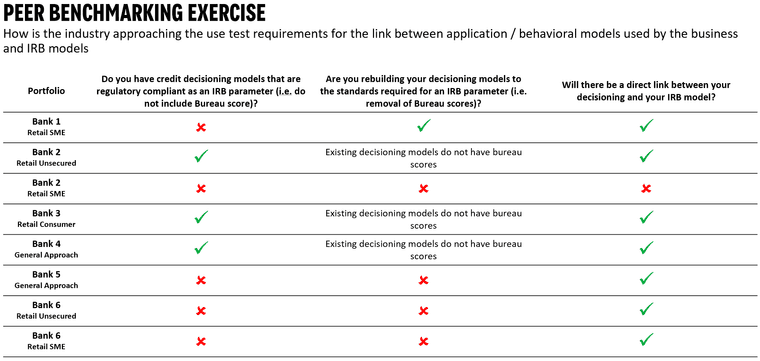

We have conducted some industry benchmarking on the topic, the results of which are shared below!

Insights we have learned:

- UK banks are linking their decisioning and IRB models to satisfy the use test

- There is a mix of approaches when it comes to removing or maintaining bureau scores in decisioning models when creating this link

- Bank 6 has an interesting approach where they will use the IRB output as the starting point for their decisioning models (essentially reversing the traditional method of linking IRB and decisioning models)

I will include the questions and answers in the comments below so you can read more about the approaches followed.

-

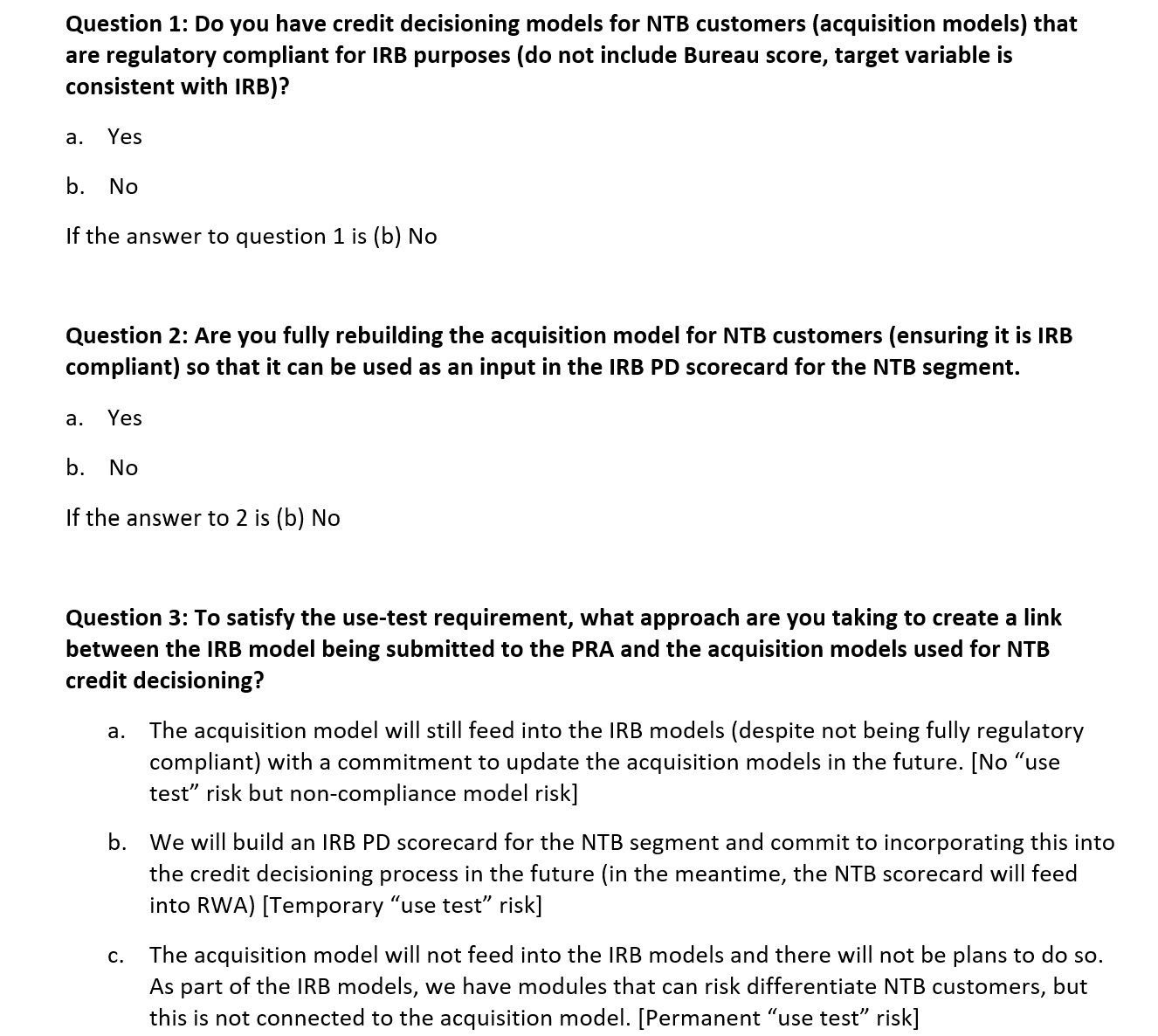

A copy of the questions asked are below

-

And below the full responses from the participants.

Answer Bank 1 – Retail SME portfolio

Q1 – (b) No

Q2 – (a) YesAnswer Bank 2 – Unsecured portfolio

The approach we are taking doesn’t really follow your flow of questions:- Applications / acquisitions can come from either New to Bank customers (NTB) or Existing Customers.

- We have recently rebuilt our scorecards we use for both NTB lending and Existing customer new lending

- Both scorecards in (2) have been developed on an operational (non-IRB compliant) definition of bad. They do not however include scores as per regulatory feedback

- Both scorecards in (2) have been calibrated to a regulatory compliant IRB DOD and used as the key drivers of PD

- Hence we believe we satisfy the Use test risk and compliance risk in our submissions.

Answer Bank 2 – Retail SME portfolio

Q1 – (b) No

Q2 – (b) No

Q3 – (c) (for NTB only)Some context:

• The IRB model includes a separate calibration segment for NTB customers <3months with Bank

• New borrowing is largely to existing customers already scored by the IRB model and hence our true “NTB” population is very small

• Default/data is very limited for SME Retail NTB restricting ability to build a separate IRB compliant model

• Use test consideration is restricted to 3months;Answer Bank 3 – Consumer retail portfolio

Answer to Q1 would be “Yes”, typically bureau scores / indices would not form part of the decisioning model as such, but they were employed heavily in subsequent strategies – limit setting, for example.

There is no obligation to have 1:1 alignment between an operational definition of bad and the full DoD as far as I’m aware – you simply have to perform a calibration of the scores to the full DoD as part of the input to the IRB PD model.Answer Bank 4 – No specific portfolio but general approach

Our approach is similar to Bank 2’s unsecured approach. We have removed bureau scores from our acquisition models. They are built using an operational DoD which is calibrated to an IRB compliant DoD and is used as a key driver in the IRB PD models.Answer Bank 5 – No specific portfolio but general approach

Q1 – (b) No

Q2 – (b) No

Q3 – (a)Answer Bank 6 – Retail Unsecured

Q1 – (b) No

Q2 – (b) No

Q3 – (a)Answer Bank 6 – Retail SME

The approach we’re currently exploring is slightly different and we intend to satisfy the use test by linking IRB models to business scorecards rather than the traditional approach of business scorecards feeding into IRB models.We will build IRB models on the ETB and NTB segments that use an IRB compliant DoD and no bureau scores. The ETB and NTB segment IRB models will then be adjusted to create new application and behavioural scorecards. The model adjustments will include the introduction of additional factors (bureau scores), an operational DoD and rejection inferencing (for application).

This approach allows for the scorecards used in strategy to include factors excluded from IRB and the flexibility to update and evolve with business needs while maintaining a use-test link.

-

If you have any questions or comments please reply to this thread!